VA Platinum Insights

Stay connected with us to receive regular updates and new blog content. Simply subscribe today!

Explore Our Latest Articles

.webp)

5 Questions to Ask a Virtual Assistant During an Interview

Unsure what questions to ask a virtual assistant or prospective staff before hiring?

More financial planners, mortgage brokers and financial advisers are adapting to better business practices with the help of virtual assistants in the Philippines.

Apart from the obvious cost-effective benefits, advisers are more productive when they hand over the administrative tasks to their staff.

If you’re reading this because you’re about to get your own virtual assistant for financial planning or a virtual assistant for mortgage broking, you’re in the right place!

Here’s what most financial planners, mortgage brokers and other financial advisers miss when conducting interviews.

A good resume should show their relevant work background, work description, education and other qualifications. If this kind of information isn’t laid out, then it’s actually a bad sign.

In addition to prodding deep into the technical content of their resumes, what you could also focus on is how compatible you are with the staff you’re hiring.

The Invitation to Dinner Test

Compatibility plays a crucial part in hiring a virtual assistant. After all, they will work with you directly and interact with you on a daily basis.

You don’t want someone who “just gets the job done”. Instead, you want someone who you can easily relate to and communicate with.

For every interview, ask yourself – “Is this someone I’m willing to invite over for dinner with my family?”

Are they interesting enough? Can I have a meaningful conversation with this person? Are they fun? Are they both interesting and interested?

The answer to that is your best bet at making the most out of your offshoring venture.

In this article, I’m rounding up my top 5 questions to ask a virtual assistant during an interview. These questions have worked in my favour, and will work for you too!

1. Ask them about their life outside work.

One of the questions to ask a virtual assistant is to have them talk about what happens outside of work and see how easily the conversation flows. Check how interesting and engaging they can be.

Ask simple questions like, “Tell me about your daily life”, “Are you married?”, “Which flavour ice cream do you like to eat?”, or “What’s your weekend like?”…

Conversations don’t work one way, so try to share some of your stories with them too!

Ask them if they have questions for you too. This way you can gauge their interest in you.

If they’re not interesting for you, then they’re not going to be an interesting person for a client, or for a client’s client.

This awfully sounds like going on a blind date, but isn’t having a good conversation the best way to start all types of relationships?

You wouldn’t get a lifetime’s worth of knowing your staff but it gives you a good insight into what your staff values are. In return, it’ll be easier for you to make them realise the value you put in your work and business.

2. How easy are they to understand?

This is more of a question you ask yourself while conducting the interview.

How well do they respond to a question?

Do they resort to using a very thick accent? Do they talk too quickly?

Do they make it easy for you to understand what they are saying?

Are they answering in a coherent manner or do they lose the subject too often that it’s distracting?

Knowing how well someone communicates doesn’t only prove their speaking skills. What’s more useful to know is the person’s ability to think on their feet.

3. Ask why they want to work with you.

Know the reason why they want to be part of your business.

Is it because of the pay?

Personally, I think that getting “a bigger pay” is not enough reason. Simply because, if someone else lures them out with more, they tend to jump ship easily.

Is it just because of career advancement?

Or, do they just want a change in the working environment?

If they come to you because of this, then you can expect that they will probably last 2-3 years until they feel the same issue and leave.

Is it because their bosses weren’t treating them well and that makes them emotionally stressed?

Is there’s no clear guidance in the company training or some of their work expectation that wasn’t provided?

Look for a stronger motivation and reassure the staff of what you can provide for them.

Your assessment should help you find staff who can stay with you for 5 years plus.

This is how you can predict how long they can work for you and what kind of commitment they’re willing to give you.

4. Ask about their relationship with their previous company.

This is somehow related to question number 3, but placed in a different angle.

What you want to know is how they talk about their relationship with the previous company.

If you get a hint that you might be operating similarly to their previous workplace, or that you share a key characteristic with them and it has become crucial to why the staff left, then it’s a possible NO for that candidate.

Here’s an example:

If an applicant tells me that they left their old job because their previous company was growing too fast, I know that they’re not a good fit for VA Platinum.

Or,

If an applicant tells me that they left because their previous company was operating early in the day and I know that I operate in the same schedule, then it’s absolutely a no-go.

Also, consider how they describe their previous company to you.

If they’re too revealing about their previous workplace, or that they easily give up classified information… you might find yourself in the same threat.

You want to keep everyone happy by understanding the staff’s expectations from you and your business.

5. Ask them about their successes.

While it’s great to hear about individual achievements, it’s better to hear how well they work with a team.

This is a personal deal-breaker for me since I work with a lot of people.

I want to hear how a person performs in a team and what achievements their team had.

Ask them, “While in a team, what did your team achieve?”

What you want to hear is not about them being better than their elbow buddy. Rather, you want to understand how they help others to be better for the team’s sake.

Asking these questions helps me and my clients get the best suited virtual assistants in the Philippines.

It’s wonderful to know how a “culturally fit” staff member works seamlessly for the benefit of your business.

Aside from the geographical distance, there’s really not much difference between hiring a virtual assistant and having someone in your physical office.

You should always treat and interact with your staff as if they sit beside you every day.

Building a good relationship with your virtual assistant that goes beyond what your business requires is a great investment. It’s an amazing workplace culture you will want to cultivate and enjoy.

.webp)

Why You Should Hire an Offshore Executive Assistant

As a busy executive or business owner, how much better would your life be if you hired someone who’s dedicated to looking after your diary, travel plans, emails, and reports?

So much easier, I bet!

And so, you must have thought about hiring a personal assistant or executive assistant.

Good decision!

As you’re on your own EA search, you probably have stumbled upon several online contents showing a buzz about hiring a Virtual Executive Assistant.

You should be thinking… “Is there a real benefit in hiring someone local versus getting someone offshore?”

Since I’m about to hire a virtual executive assistant (EA) myself, I’ve written this article to explore the whys of hiring offshore executive assistants.

While doing my research, I came across this very interesting news…

As reported in the Australian Financial Review in February 2018, Ernst and Young now have 38 Executive Assistants in Manila working for executives in Australia and New Zealand. Ernst and Young started a trial in 2016 with 20 EAs in Manila and the number has been steadily grown. 15% of Ernst and Young’s EAs are now hired offshore!

So what made them (and soon…me!) hire an offshore and virtual executive assistant?

Here’s what I have to say…

1. Scope of responsibility

Personally, I’d be happy to employ someone very organised and resourceful, has advanced skills in MS Excel, can handle document preparation, and take on tasks confidently in a timely manner.

Specifically, I need my EA to:

- Manage my travel schedules

- Process and keep track of my expenses

- Coordinate my meeting schedules

- Email management

- Compile and create presentations

Unsurprisingly, these are tasks that don’t require physical presence. So having someone offshore to take care of them isn’t much of a worry.

Also, tasks are easily delegated and communicated over email, Skype, Zoom, or whichever communication tool you prefer to use.

The catch is, it’s absolutely important that you make clear and concise instructions. This way you may anticipate that the work you want to be done is done well.

Of course, there are downsides to not having a local EA,

Basically, A Virtual EA cannot…

- Find a venue to run an off-site meeting

- Facilitate print jobs

- Pick or deliver things

- Attend events or meetings on your behalf

But if like me, you only require support that does not involve the tasks above, then hiring a virtual VA might just be the right decision to make!

2. Availability

Well, the point of hiring an EA is you want someone to help carry on tasks that eat away your time.

You might think that availability is a serious concern if you hire someone offshore, but it’s fascinating to know that it’s not.

In a study conducted by the Stanford University School of Business, it has been revealed that those who work from home (or remotely) were 13% more productive than those who are in the office.

This goes to show that as long as you clearly define your work hours, you can get in touch with your virtual executive assistant as often as you can with a local EA!

3. Monitoring Work

Getting the job done well is essentially what I value the most.

Because of the limitation of interaction you have with a virtual EA, there might be lesser opportunities to track a virtual EA’s work.

The good news is, with the help of tools for time-tracking, such as TimeDoctor, Toggl, Qbserve, etc. you can remotely observe how your staff spends the day!

4. Cost-saving

On the latest Payscale report, it shows that a local EA in Melbourne earns an average base salary of $5,755 AUD per month.

Meanwhile, an offshore EA from the Philippines will normally cost you around $2,000 AUD – and that already accounts for HMO, internet, facilities, and even free meals!

So how much difference are we talking about, cost-wise? Holy smokes! We’re talking about more than 50% savings!

Plus, it’s no secret that the cost of living in the Philippines is much cheaper compared to Australia. That said, even though your savings is significantly large, your staff still enjoys working for a better value compared to other white-collar jobs in their country.

4. The right talent

Regardless if you’re looking for local or offshore talent, you are still to undergo the pains of recruitment.

As for the Virtual Executive Assistant hunt, there are different strategies you can use to find the right talent.

But let me narrow them down into 2:

Do it Yourself

Pretty much self-explanatory and would involve a lot of your time. If you want a hands-on approach to finding the best person for the job, then this might be a route you’d want to take.

You can always post your hiring notice in Upwork, Odesk, etc., and pray that someone good reaches out to you.

Have an Offshore Virtual Service Provider

This helps a lot, especially when you want to make sure that the people you get are already professionally screened. You have a better chance of finding the right talent and personality (including background checks) to support you.

Additional care is also provided to your staff to ensure that the quality of work is monitored, even when you are not around. Security measures are also covered by the company to ensure that there are no concerns with data breaches and confidentiality.

Now, does it really make a lot of difference if you hire offshore? I say YES – and all for the right reasons! In fact, when bigger companies try to get into the virtual EA trend, it just goes to show that there really is more to gain in this option.

.webp)

Is Your Business Safe from Privacy & Data Breach?

As the cost of running a financial services business in Australia increase and ASIC places heavier compliance obligations on businesses, there are very few options to save money while improving customer service.

The most obvious strategy businesses are taking advantage of is using offshore businesses like VA Platinum.

So, are you using overseas administration services as part of your business?

If yes, and you haven’t a clue about how the Australian law works for data privacy, or do not know how it should be implemented in your operations, below, I’ve given a step by step of what you need to know and how you can stay on the right side of the law.

Seriously, this could save you from some serious penalties and possible jail time.

And I don’t mean to scare. Laws are meant to be intimidating, and so we have to be mindful and respectful of them to avoid the backlash of the looming “or else”.

Firstly, let’s do a bit of background research….

What is APP 8 and why does it matter?

The Australian Privacy Principle, or APPs, is a 13-point framework of the Australian Privacy Act of 1988. The Privacy Act was created to protect and regulate how personal information is handled. In its essence, it safeguards the rights of individuals and strengthens community trust in businesses and agencies.

Personal information is defined as…

“Information or an opinion, whether true or not, and whether recorded in a material form or not, about an identified individual, or an individual who is reasonably identifiable.”

Personal information is, but not limited to: an individual’s name, signature, address, telephone number, date of birth, medical records, bank account details, and commentary or opinion about a person.

All APPs are created to guide us with the proper way of handling personal information, for a number of specific scenarios. APP 8 specifically outlines the cross-border disclosure of personal information.

APP 8 particularly details your legal obligations if you are utilising overseas or offshore operation that involves passing around personal information.

Personal information is defined as…

- If you use Dropbox, Google Drive, OneDrive, or other similar file storage facility that your offshore staff access.

- Where you provide access to your customer database such as Adviser Logic, Xplan, Midwinter, etc.

- Where you send a fact find or scope of advice document offshore to prepare advice documents such as a Statement of Advice.

Key Points

You can find the full inclusions of APP 8 through the Office of the Australian Information Commissioner.

For the purpose of simplifying the points under this principle, I’ve outlined them below:

1. Implement Data and Privacy Security Measures in your office

If your business discloses personal information to an overseas recipient, you must take reasonable steps to ensure that the recipient does not breach the APPs in connection with the personal information.

This means that you have to implement an anti-recording policy in the office or use software that effectively keeps people away from accessing personal information outside of work.

2. Acknowledge accountability for Data & Privacy Breach

An Australian entity may still be held accountable for the practices or acts of an overseas recipient which result in a privacy breach even if they have taken reasonable steps.

However, the Office of the Australian Information Commissioner (OAIC) will take into account the reasonable steps followed when resolving the matter.

3.Provide proper disclosure to clients

Proper disclosure must be issued to the individual for them to effectively grant consent.

Following point number 3, I have asked my clients to include a disclosure to clients with regards to using offshore staff through us. I created the following text to put inside their respective Fact Find and Privacy Policy (or in their FSG and SoA):

“Some of the information (including health information) collected by us may be disclosed to employees or contractors of [YOUR COMPANY NAME] outside of Australia. You consent to your information being disclosed to a destination outside Australia for this purpose, including but not limited to Cebu, Philippines.”

For those wanting a smaller disclosure, I encouraged them to use what one of our VA Platinum clients has included in their privacy policy that every client must sign.

“Note: we do utilise some overseas administration.”

Either way, I recommend that when using offshore staff, you must include a suitable disclosure that is easily identifiable in a document that the client signs off on.

4. Make sure that personal data is used strictly for its primary purpose

The Privacy Principle sets out that the business must only disclose personal information for the primary purpose it was collected unless an exception to this principle applies. An Australian entity is only allowed to use or disclose personal information for a secondary purpose (defined as the non-primary purpose) in the following situations:

- where the individual grants consent;

- where the law requires disclosure; or

- where it is “reasonably expected” that the Australian entity would disclose the information for secondary purposes.

In these circumstances, the Australian entity must justify its actions and satisfy the Office of the Australian Information Commissioner (OAIC) that its disclosure was reasonably expected.

In summary, it’s incredibly easy to comply with Australia’s privacy laws when using offshore staff in our overseas outsourcing businesses.

You simply need to disclose to customers that their data may be sent offshore and only used for the purpose intended and have the client sign-off that they grant you permission.

Easy peasy!

.webp)

7 Mistakes Business Owners Commit When Working With Virtual Assistants

First, congratulations for dabbling into the world of offshoring! Whether or not you came to VA Platinum to get your virtual assistant for financial planning, a virtual assistant for mortgage broking, or an executive assistant, I like to commend you for taking a step towards freedom by working with virtual assistants.

If you are new to offshoring, you are most likely to find yourselves questioning your decision due to unfamiliarity or culture shock.

I totally relate to waking up all sweaty and uneasy when I first started. Back then, I did everything on my own, searching from volumes of profiles in Upwork (formerly known as Odesk).

I remember having to deal with at least 15 people to find someone to replace a staff who suddenly ran AWOL.

Thankfully, I overcame it after learning the hard way.

I’m no stranger to the overwhelming looks of advisers and business owners coming to me to get some kind of assurance that they’re doing well with their staff.

Because of this, I was able to recognise what goes wrong in the mix and I’m happy to have figured out the ways to correct it.

So here I am, sharing the top 7 mistakes I find advisers and business owners commit when working with virtual assistants.

Let’s dive in!

1. Only hiring (1) staff

It’s settled that an offshore virtual assistant costs 1/3 of what an office staff earns in Australia. If it is a matter of cutting costs, hiring 2 staff will still help you save.

Plus, there are so many benefits in getting 2 staff right off the bat:

Training

Let me tell you an amazing discovery – staff train each other.

What I realised working with virtual assistants in the Philippines is that when they are paired up; they learn, grow and share knowledge together as one awesome unit – even without your supervision!

They are more confident, attentive and engaged because they know that they’re responsible for checking each other’s work. They work independently, but interact as a team.

Back Up

Honestly, this is a fail-proof way of assuring that you always have a staff to support you in any given day.

If there’s an emergency situation and one staff member is away, you can simply endorse the work to the other staff you have present.

Let’s say, for some reasonable decision one of your staff member decides to quit – you won’t feel too pressured about training new team members because your tenured staff member can take care of the training.

Faster Task Completion

Having 2 or more staff makes the workload lighter. Staff pay attention to their work better because they have adequate time to complete their task and finish more in a day.

2. Starting with a Part-Time worker

If you want to keep the skilled and talented staff, please stay away from hiring part-timers.

It’s going to be a waste of your effort, time and resources.

Imagine having to train people who simply pop in and out of your business!

You see, part-time workers will not invest their 100% attention with you, as your relationship is limited. They can also be working part-time for someone else, and I hope it’s not for a competing business or else, your business might be at risk!

The bottom line is – if you want your staff to be involved in your operation for the long haul, you have to attract them with stability.

3. Being Task-Oriented with Staff

Most business owners put up a wall between them and their staff. They take the work relationship to the bare minimum level of just handing over tasks and evaluating results.

I believe that I’ve emphasised this in almost all of my blogs but what I want you to do is to connect with them on a social level.

Leaving out that “human connection” dampens your work relationship and does not add value to either you or the staff’s life.

I encourage all my clients to kick off their initial meeting with conversations that help the staff member understand you as a person and your goals as a business owner/adviser.

You have to lay a good foundation with your relationship with the staff because after all, they will be a part of your success.

4. Treating your staff like you treat Australians

I might be generalising (a lot) – but we, “the Aussies” are the chip-in-the-shoulder bunch. We’re not used to seeing people being so warm and friendly that we get surprised when we meet people from different cultures.

People in Cebu, specifically are the most fun and friendly!

Social connections are important to them. It is one of the most important traits that business owners or advisers fail to acknowledge.

Be friendly and sincere. You will be amazed at how you can connect with them instantly.

5. Hiring the first person they “think” is good for the business

Just because you find someone close to what you’re looking for doesn’t mean that you should close your door to other prospective staff.

The job of a good virtual assistant service provider is to give you the best possible staff that will help you grow your business.

In VA Platinum, we let your staff take aptitude tests and personality tests and even get their DiSC profile upon your request so we can be sure that they are culturally adept to work with you.

Trust me, the clients who have the most “culturally fit” staff took their time in choosing!

So say NO, if you feel that they are not the best fit – you’ll eventually find the right ones, and I’m sure they will be worth it!

6. Making tasks/systems before hiring staff

Do not create/document processes and systems before hiring your virtual assistants.

I recommend that for the first 2-3 months of working with your staff, you arrange training calls as often as you can. Avoid emailing them or Skype-ing them what you need to get done. Instead, have your staff record all your training sessions and ask them to create the processes by themselves.

This way, you’ll know how they understood it from you, and in return, you can coach them to change what they might have missed out on.

7. Giving all tasks at once

Do not drop tasks to their laps all in one go.

Let’s say, there are 25 tasks you need them to take over. Arrange it in the order of priorities. Train them with the first 5 tasks, check back their work and have them do it again until it’s perfect.

Once you’re confident about having them do it on their own, give another batch of 5 tasks. Do this until all the tasks are handed over to them.

Dropping everything in one go will overwhelm your staff so much that it might make them feel so burdened. Doing everything in a rush will also result in poor output due to the lack of guidance on your part.

So, for them to do a fantastic job, you have to agree upon a good pace where learning and coaching are possible.

If you have been guilty of committing a few mistakes I have mentioned above, bless your heart! I hope you find this article useful to turn things around.

I’m sure you’ll be interested to know more about what you can do to improve your offshoring experience.

Did I miss something? Let me know in the comment section below!

5 Things to Expect When Working with Filipino Virtual Assistants

“What is it like working with staff who are thousands of kilometres away?”

I get this question a lot.

A lot of financial advisers, mortgage brokers, real estate agents, and business owners enlist the services of virtual assistants these days.

Those who haven’t, are curious about what to expect.

People worry that the cultural gap is too wide.

However, working with offshore staff is not complicated.

I’ve experienced so many benefits working with virtual assistants in the Philippines that I didn’t mind not having a physical office or not having my staff physically in front of me.

In fact, I preferred it.

So, here’s what you should expect when working with virtual assistants from the Philippines:

1. Expect a superstar

You’ll be working with a superstar staff member and this should be the minimum expectation!

If you approach it with low expectations, you won’t give enough time and effort into ensuring you hire the right person.

I’ve emphasised in previous blogs how important it is to take time in interviewing applicants and finding the best person for the role.

This way, you’ll be investing time and energy in training and developing staff who are dedicated to their work and produce results.

Put enough time and energy into your virtual assistant and you will get someone who will surpass your expectations.

They will be productive for 7.5 hours a day.

I know this because Time Doctor monitors the work being done!

Staff are focused on their tasks and output is maximised.

2. Expect to treat them like they’re right there with you

Sure they’re 4,000 kilometres away but hear me out.

You should develop a great relationship with your virtual assistant.

Say “good morning” and “good night”. Discuss the weekend, share a joke!

Your virtual assistant has likes, dislikes, interests, and personality traits. Get to know them as you would their Australian counterpart.

Heck, plan a working holiday! If at all possible, visit the Philippines.

Make an effort to understand how your virtual assistant lives. Get to know what day-to-day life looks like.

Understand the economic environment, the transport system, and everyday things that your Filipino staff experience that is different from Australia.

This should give you a glimpse of the world through their eyes.

Here’s a scenario:

Your virtual assistant tells you that they need to go to the bank and they’re gone for an hour.

You’d be frustrated right?

As an Aussie, we’re used to being served in 5 minutes.

Who needs an hour to go to the bank?

What you don’t know is that the lines are RIDICULOUSLY LONG at banks in the Philippines.

I’m not kidding when I say that a bank queue goes out the door…. and around the corner.

Understanding how your staff live and getting to know them will give you a better perspective on how they work.

Embrace a personal connection.

3. Expect a lot of video calls

Arrange video calls with your staff, at least during the first few months with them.

I encourage clients to spend at least an hour during the morning for training and at least two half-hour sessions during the afternoon for Q and A when working with a new virtual assistant.

Whilst it can be done over the phone, video calls are more effective.

About 90% of communication is non-verbal (body language and tone), so how you present is actually more important than what you say.

I’ve spoken to virtual assistants who have misunderstood my message because they couldn’t see my face!

As soon as we started using video as the main tool, communication became much easier.

Lesson learnt: video call your virtual assistant through Skype and have face to face conversations as often as possible.

4. Expect to be more productive

This is the biggest win when working with virtual assistants.

Previously when I had an office and lots of staff sitting nearby, I would get interrupted every 5 to 10 minutes with a question.

I could go through a whole day and not finish a single 30-minute task because of never-ending interruptions.

When your momentum is disturbed, it usually takes a few minutes to get back into the groove.

I would go to a cafe or a park with my laptop, turn off my phone, and work there so I wouldn’t get distracted.

That was a crazy work set-up, and I’m so glad I’ve moved on.

Thanks to my virtual assistants, I now work from home and help other business owners enjoy the same benefits.

I’m more productive and I’m happier!

I have time to play with my son, exercise, read a book…

I know a lot of business owners who use our virtual assistant services also feel the same way.

5. Expect fun

“There is little success where there is little laughter.” – Andrew Carnegie (Entrepreneur)

Honestly, the fun and energy I’ve experienced from Filipino culture outweigh anything I’ve experienced in Australia.

We have breakfast in the office every morning, and I have staff who dance and sing while we’re eating!

They’re a fun and quirky bunch. You can feel their positive energy even through the computer screen.

This amazes me.

What is more amazing is how contagious it is. The positivity and liveliness are evident in everything they do, and it rubs off on you.

It lifts you up. It’s the type of energy you’d want to feel when working with staff.

This is why, I think, they make awesome staff members.

The benefits of getting virtual assistants are life-changing.

Not only for your business, but you also get a fresh and different life perspective by getting to know and understand your offshore staff.

Although you are thousands of kilometres away, expect the best from your virtual assistants and you’ll appreciate the best staff you’ve ever had.

These are my top 5 observations, but I’m sure that other business owners who work with Filipino virtual assistants have more to add.

Have you worked with a virtual assistant yet? Contact us.

.webp)

How to Grow Your Advice Practice with Offshore Virtual Assistants

Many advisers start off by structuring their advice practice business through trial and error to see what might work.

But what if I tell you there’s a way to skip the experiments and proceed with a structure that’s proven to work?

Good stuff, right!

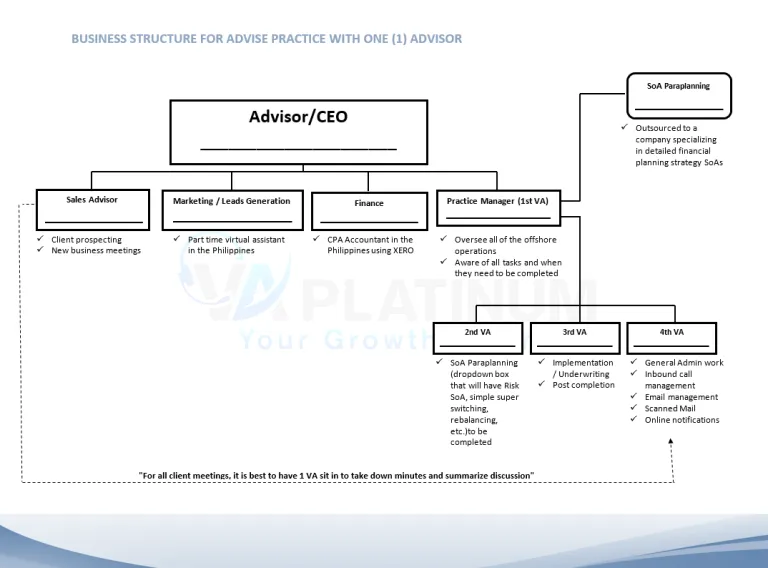

In this article, I provide you with the ideal business structure specifically tailored for Advice Practices with One (1) Adviser and multiple support staff.

Building a business structure is critical to any growing business. It’s the framework that dictates job roles and decision-making responsibilities. It helps the business move forward with the least expense and smoothly.

Let’s face it, even though you have the business vision, there are roles you cannot force yourself into. It’s good to be an enthusiastic jack-of-all-trades, but juggling all tasks might stall your growth or leave you burnt out.

Understanding your strengths and weaknesses is a critical insight into running your company.

Direct your focus on doing what it is that you do best and find the right people with the right talent to assist you.

Whether you are in Financial Planning, Mortgage Broking, or an Insurance Planning business, this structure will help you strengthen your own virtual workplace.

Fig.1

Below, I share with you how each role is ideally incorporated into your business practice.

Adviser/CEO

Being an adviser is a whole combination of responsibilities in itself. Other than servicing clients by giving professional financial advice and solutions, you are also managing client relationships and maintaining the business practice.

Additionally, as the highest-ranking executive in the company, you are responsible for making major business decisions, managing the overall operations and resources of the company, planning overall growth, delegating tasks to other managers or various departments, and lastly, hiring staff.

1. Sales Advisers

This department is responsible for generating and attracting new clients whilst making sure that the services you offer are well-presented and well-received.

In the advice practice, sales advisers focus primarily on client prospecting and building client relationships.

While you are responsible for giving the actual professional advice, your sales adviser is responsible for onboarding new clients and making sure that they understand your process and practice. They are also responsible for initiating new business meetings and finds you a way to build and widen your client network.

In our company, my business partner Ed Arguelles and I are in the frontline of building client relationships. I do most of the business management and Ed takes care of the onboarding for client prospects and new clients.

2. Finance

This department tracks the finances and ensures that any gains or losses are appropriately managed and circulated.

The Finance Office role can be filled in by an offshore staff – ideally, a Certified Public Accountant in the Philippines who is knowledgeable about the use of XERO.

3. Practice Manager

This department oversees and manages all offshore operations.

Your Practice Manager is your 1st Virtual Assistant, there to take care of coordinating and delegating tasks to other team members. This staff will also be your main point of contact for any admin-related concerns or tasks.

The Practice Manager is also responsible for reviewing staff performance, training, and coaching.

Under the Practice Manager, there are the following available roles:

SoA Paraplanning

You can get SoA Paraplanning outsourced to a company specialising in detailed financial planning strategy SoAs. This is the best option if you’re not ready to hire an in-house or offshore full-time paraplanner at the moment.

It’s easy to find firms that offer this service. A simple “Googling” will give you a great number of options. The fees vary depending on the number of SoAs you need in a week and the number of hours the paraplanners allot to it.

Your practice manager will handle communication to any outsourcing firm of your choice and make sure that the documents are complete, accurate, and are compliant.

General Admin Virtual Assistants

You would need additional staff to focus on specific aspects of administrative work. Having enough people in your team allows room for backup, in case some of your staff are not able to come into work.

Here’s my suggested task allocation for 3 more staff:

2nd Virtual Assistant

Your 2nd VA is your SoA Paraplanning support. This particular staff will take care of Risk SoA, simple super switching, rebalancing, etc.

Here are other tasks they do:

You would need additional staff to focus on specific aspects of administrative work. Having enough people in your team allows room for backup, in case some of your staff are not able to come into work.

- Updating client paper and electronic files, ensuring that they are compliant

- Completing, checking, submitting, and processing the necessary application forms

- Preparing basic SoA’s such as life insurance only and superannuation rollovers (for strategy-based SoA’s we can establish a relationship for you with specialised SoA paraplanners)

- Preparing Record of Advice

- Entering client data into financial planning software

- Liaising with fund managers, administrators and life companies regarding client’s financial situation

- Assisting with research into client recommendations

- Monitoring stationery, ensuring always sufficient supply and not out of date

3rd Virtual Assistant

Your 3rd VA will handle administrative tasks relating to Implementation and Underwriting. They will also take care of handling any post-completion process and concern.

Here are other tasks they do:

- Contacting clients for outstanding underwriting or admin requirements, contacting insurers when changes need to be done on the application (name incorrectly spelled, DOB, address, etc.), making sure policies go into force as soon as possible

- Ensuring regulatory compliance of Sales Paraplanners and Advisers

- Reviewing and submitting the application

- Verifying all documents are completed/signed fully and correctly

- Scheduling client appointment

- Managing medical requirements

- Organising/following up on any outstanding requirements (e.g., financial documents, superfund details, rollover forms) if applicable

4th Virtual Assistant

Your 4th Virtual Assistant will handle both inbound and outbound calls, email management, scanned mail, online notification, and other ad hoc administrative work.

- Managing incoming emails, mail, faxes & message bank

- Assisting with client appointment booking, researching into the client, recommendations, quoting, processing, filing, and preparing client documents

- Liaising with fund managers, administrators, and life companies regarding client affairs

- Client service e.g. attends to client query and request

- Maintenance of client databases and creation of files

- Assist with management reporting on a monthly basis or as required

- Processing applications, renewals or changes to existing client records

- Ensuring regulatory compliance

- Data Entry

I also added an auxiliary role to support sales. I have made this department a stand-alone, granted that the task can be one-off or outsourced part-time, rather than full-time.

4. Marketing & Lead Generation

Basically, this department is responsible for handling Digital Marketing campaigns and lead generation.

Digital Marketing has already been a constant effort of business who wants to keep their practices social media relevant.

Your Marketing & Lead Generation department can be handled by a part-time Virtual Assistant in the Philippines who has knowledge of different Digital Marketing campaigns. It’s a great bonus if you can find someone who knows how to manage your website and produce content.

Part of the task includes getting email contact from LinkedIn, Facebook, or other sources.

Other tasks may include:

- Updating the website feature without the need for coding

- Building email marketing campaigns

- Creating and managing social media accounts

- Writing digital content for blogs, articles and other social media posts

- Writing, publishing and managing blog content

- Generating reports from MailChimp, Facebook and Google Analytics

For all of you planning to start your own advice practice, it is important to start with a firm foundation. However, as your business develops, it’s just natural to make adjustments to adapt to any change that comes with growth.

Exploring Global Talent Solutions? Start Here.

Let us know about the roles or tasks you’d like to offshore in your business. Within a day or two, we’ll get back to you with insights and solutions tailored to your business.